|

|

|

|

|

|

|

|

Merchant Account TypesMerchant Account ProvidersNews & AdviceMerchant Account Tools |

Print Print  Email Email Merchants eye mobile phones to transact card paymentsMerchants on the go have more options today when it comes to processing credit card transactions, with smart-phone credit card processing applications offering the potential for higher sales, faster collections and fewer bad debts.

Users of iPhone, Palm Treo, HP iPAQ, Sprint Moto and other phones can purchase credit card processing applications that allow them to take credit card payments and transmit them securely without any carrying add-on magnetic stripe readers or other technology. These applications free merchants from their offices, land-lines and special processing equipment, potentially making business easier for merchants and employees who frequently work remotely. The applications are part of a broad-based effort by smart-phone manufacturers and application developers to push more business-related functions to all-in-one smart phones, making them more attractive to business owners and corporations. The appeal of the iPhone as a business device drove Derek Del Conte and his business partners at InnerFence, an iPhone application development company, to develop an iPhone credit card terminal. Businesses can use applications for employee tracking and increasing efficiency, he says. "So we looked at it from the perspective of what applications would help drive up revenue, and we came on the credit card terminal because being able to take payments in more places helps drive up revenue, and collecting revenue on site means you don't have to deal with collection issues." The terminal's technology may not be revolutionary, but it is "exciting," says Shyam Krishnan, a technology analyst with Frost and Sullivan, an international consulting firm. Significant barriers remain to widespread adoption. The terminal applicationss being developed for iPhones and smart phones "will need a lot of time to remain etched in consumers' memories," he says. "The economic situation has hit the information and communications technologies industries across different domains and people are holding back spending on smart phones."

How they work There are two reasons:

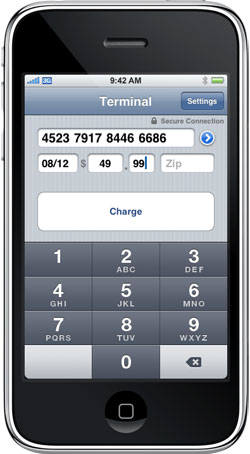

To initiate transactions, merchants enter customers' credit card numbers, expiration dates, ZIP codes and transaction amounts on iPhone touch screens or smart-phone keyboards. Some applications offer the capability to enter other data, such as a credit card security code, additional consumer information, an invoice number and a product description.

Once the merchant enters the information and transmits it, the payment goes through a secure payment processor such as Authorize.net. The merchant then receives confirmation that the credit card number is good and that the charge has been processed. For Gregory Perez, owner of Twiin Photography in Indianapolis, use of the iPhone credit card terminal eliminates collection problems and may increase sales. "When I was on the road previously, collecting credit card payments through the knucklebuster manual swiper could be rough because I didn't know, on site, if the card was going to go through," he says. "Now, if the first card doesn't go through, I can ask for a second card and avoid trying to collect later." For small business owners such as Perez, the availability of on-site credit card processing can boost sales, as consumers are more willing to spend with plastic. Many merchants find that adding the option of credit card payments increases overall sales and the amount of individual transactions.

Costs and security

Because applications adhere to the PCI Security Standards Council's latest data security standards, Del Conte says they are as secure as if you entered your credit card number on a Web site with encrypted security, or used a store's manual card-swipe terminal. "Security is not something we take lightly, so we spent a lot of time on it," says Del Conte. "The communication between the phone and Authorize.net is encrypted point to point," he continues. "When the merchant logs into the app on the iPhone, it is done through a user name and password that is stored in a key chain on the iPhone that is also encrypted. The application does not store consumers' credit card information. There are a lot of industry rules around that. So when the merchant taps 'Send,' and the information is sent to Authorize.net, that information goes away and can't be accessed again on the phone."

A glimpse of the future The market for trackin consumers' financial records via smart phones expands as companies develop digital wallet applications. Dan Grigsby, who blogs about iPhone apps at Mobile Orchard, an iPhone development blog, sees a future in which consumers and merchants can send and receive payments on their smart phones. Current smart-phone credit card processing applications target too narrow a niche to impact the credit card processing industry, he says. Krishnan sees an increased market for applications such as these once the economy recovers. "As the economy picks up and as people decide to spend more on high-end items, these applications will come into reckoning," he says. "This would mean lesser usage of credit/debit cards as consumers view the phone as a one-stop tool for all of their requirements. It could be faster, not necessarily more secure than current systems since the networks will have to be fortified with security built just for this purpose." Updated: February 3,2025Comments or Questions, Library of Stories

|

|||||||||||||||||